by Emerson Nafziger, ILLINOIS Extension Agronomist

March rainfall in Illinois ranged from normal to a couple of inches above normal, but the last week of March and first week of April have been relatively dry, and field operations are getting underway. The April 6 NASS report indicates that there were 3.1 days suitable for fieldwork in Illinois during the week ending on April 5, but no planting was recorded. As is often the case in early April, soils are wet over most of the state.

The 4-inch soil temperatures at 10 AM have been close to 50 degrees in southern Illinois, and over the past week they have increased from the low 40s to the mid–40s in central and northern Illinois. The forecast is for a return to cooler weather later this week, and possibly to wetter conditions as well. Such “yo-yoing” is normal for April, and it often brings up questions about what to do when the weather forecast is for conditions to deteriorate as planting approaches. Do we plant or do we wait?

There is no question that the ideal is for seed of both corn and soybean to be planted into soils that are relatively dry, and that are warm (and warming) enough to allow germination and emergence to get started quickly, and plants to grow steadily after emergence. The most recent example of the benefits of this was in 2018, when planting was delayed until May, then May weather was very warm, and the crops “never looked back” on their way to new yield records. In 2017, early corn planting was followed by a week of cool, wet weather, which led to a lot of replanting. The replanted crop often yielded more than the first crop, almost certainly because it had warmer conditions under which to germinate and begin to grow.

Having soils stay dry after early planting into cool soils is much better than having them turn wet: the germination process is very slow at low temperatures, so seeds will bide their time until soils warm up, and dry soils are a safer place to do that. If it turns wet, seeds will last longer in cool soils than in warm ones, both because low temperatures delay the germination process (and the demand for oxygen), and because colder water contains more oxygen than warmer water. Still, seeds that spend a week or more in wet soils at temperatures in the low 40s are subject to “imbibitional chilling injury” that can mean abnormal growth and poor emergence even if seeds survive. This is considered more of a problem in corn than in soybean, in part because more soybean seeds than corn seeds tend to die under such conditions and so don’t show those symptoms.

Planting date

Now that we’ve passed the first week of April, plantings of this year’s corn or soybean crops from now on can’t be considered “very early”, but the message from some agronomists about the need to plant soybeans as early as March continues, and more producers are choosing to begin planting soybeans before they begin planting corn. With planting date responses for the two crops essentially identical on a percentage basis, which crop to start with is more or less a tossup. The deciding factor in that case should often be which fields are ready first. Fields where soybeans grew last year will often be in good shape to plant earlier than those where corn grew, and that may mean planting some corn first. It certainly makes little sense to plant soybeans when it’s too wet just to plant them earlier than corn.

I have mentioned before the possibility that soybeans planted very early—in March or early April—might occasionally yield less than those planted in late April or early May. I dug up some data from a study that we did back in 2001–2003 in which we started planting as soon as we could (without planting in mud) using different seeding rates and varieties with different maturities. Figure 1 shows yields from this study, with planting date averaged over sites. Yields were not as high as we’d expect today, but the earliest planting yielded the least of all the planting dates. This was not due to low stands, with the exception of the Urbana site in 2001, when it froze (temperatures in the upper 20s) just as the crop was emerging, and about half of the plants from the first planting date were killed. We had five sites in southern Illinois, where average yields were even lower, but the earliest planting there (average of April 15) yielded less than either the early May or late May planting.

Figure 1. Soybean planting date responses over nine trials in central/northern Illinois, 2001–2003.

Figure 1. Soybean planting date responses over nine trials in central/northern Illinois, 2001–2003.

While changes in seed quality, spring weather, and perhaps genetics have lowered the threat of such losses from very early planting, we can’t rule out the possibility that planting soybeans in March or early April may not always maximize yield. That’s not necessarily because of stand loss from frost or wet soils. Frost can typically kill soybean plants only in a one- or two-day window as the plants are breaking through the soil surface. Frost that occurs after the first two leaves unroll can kill the growing point, but then buds will break and form (usually two) new stems. Most low stands in soybeans follow heavy rainfall soon after planting, and chances of that happening are not closely tied to when the crop is planted. Instead, the evidence is that low temperature stress during early growth may limit node and seed number per plant, therefore limiting yield potential. The fact that the earliest planting in northern Illinois responded so much to seeding rate reflects the fact that these plants did not have as many seeds as those planted later.

One of the incentives to plant soybeans very early is that some seed companies provide free replant seed. I do not know if “free” includes the cost of seed treatments (for replant seed) that are commonly applied to soybean seed at the point of sale. Soybean seed meant for early planting is often treated with several plant protectants, including ILeVO® for decreasing the incidence of SDS. That disease is generally considered more likely to be a problem when soybeans are planted into cold soils.

The debate among agronomists regarding the merits of planting soybeans in March or early April—before the start of corn planting—is still alive, but focusing on “corn versus soybean” as if it’s a contest mostly misses the point. Both corn and soybean benefit from early planting most of the time, and both face similar risks when conditions deteriorate after we plant early. We shouldn’t decide when to start planting or which crop gets priority based on how “tough” each crop is or on trying to prove someone wrong. The goal instead is to minimize risk and to maximize yield potential. The 2019 growing season was such that that penalty from late planting was relatively less for soybeans than for corn. That doesn’t mean that corn should get first planting priority this year. Both crops should get priority, with actual planting order determined by factors such as logistics, how fast fields dry, and crop insurance.

Recent research on how both corn and soybeans respond to planting date in Illinois is summarized below in Figure 2. I’ve shown both lines on the same figure before, but here I’m including the actual data for both crops along with the curves in order to show how variability changes as planting is delayed. While we did not try to plant soybeans before mid-April in this study, note that hardly any of the April soybean plantings produced less than maximum yields in these trials. With mid-April plantings yielding the same as late-April plantings, it seems unlikely that yields from planting in March would have been higher than those from planting in April.

Figure 2. Corn and soybean planting date responses in Illinois trials. Each trial included four planting dates, and yields were converted to percent of the maximum yield in that trial.

Figure 2. Corn and soybean planting date responses in Illinois trials. Each trial included four planting dates, and yields were converted to percent of the maximum yield in that trial.

Unlike soybean, the earliest planting dates for corn did not consistently produce the highest yields in the trials shown in Figure 2. This was not due to poor stands or frost damage, but was the result of growing conditions later in the season, and was more common when yields levels were lower. It’s difficult to untangle what happened in each of these, but in a few cases the early-planted crop experienced cool temperatures in May that might have lowered yield potential. The growing season was relatively dry in some of these sites as well, and small differences in rainfall timing could have favored the crop that was planted a little later. We added an additional planting date in mid-March in the very dry spring of 2012, and lost about half of the stand to frost during the second week of April.

Planting depth

Recent developments in automated depth and down-pressure controls on planters have brought new attention to the issues of planting depth and seed placement. While research done over a few sites often identifies a “best” depth, such results don’t very well predict what the best depth will be in a given field the next time. We can guess the best planting depth about as well as we can guess the weather, although the depth decision is easier in some soils than in others. Most studies include planting both too shallow and too deep, with a few depths in the middle, and results typically show, to no one’s surprise, that it is better to avoid planting too shallow or too deep.

An additional feature available on some planters is a sensor for soil moisture coupled with the ability to vary planting depth based on where in the soil there’s enough moisture to get germination started. This has potential for dry areas where soil moisture frequently is low during the planting season. But I think we need to be cautious with this in the eastern Corn Belt, where soils are heavier and where heavy rainfall after planting and before emergence is a much serious threat to stand establishment than dry soil at planting. Planting deeper means that emergence almost always takes longer, and that means more chances of having problems related to wet soils and surface compaction (crusting) as soils dry out after they get wet. In practice, I think this means that planting 3 inches deep or deeper in most Illinois soils (sandy soil is an exception), even if that’s where soil moisture is adequate, has a better chance of lowering stand counts than it does of increasing them. Most corn seed has the ability to emerge from 3 inches deep if soil conditions are good, but when soil conditions deteriorate after planting, those three inches can turn onto an obstacle course for seedlings. That can compromise stands and stand uniformity, both of which are needed for getting the highest yields.

Today’s planters do a good job of pressing soil against seeds for the sides and above, resulting in good seed-soil contact without compacting the soil above the seed. Good seed-soil contact forms a conduit by which water can move through the soil into the seed as germination begins. That effectively enlarges the soil volume from which seeds can draw water, which means that even soils with lower moisture content often have enough water to allow germination, especially in silt loam and silty clay loam soils without clods. Clods form when soil that was tilled when it was wet dries out. With less tillage and less time between tillage and planting today, soils often do not to dry out very much before planting. As a result, uneven stands due to uneven soil moisture is relatively rare in most Illinois fields. Those who can’t remember when they last saw uneven stands due to uneven soil moisture at planting—that is, times when some seeds had to wait for rain before they emerged—might have reason to question the advisability of having soil moisture determine how deep seeds are planted.

So where, between too shallow (let’s say one inch) and too deep (3 inches in most soils) should we plant? Soybeans planted in the first half of April with soil temperatures (2 inches deep measured at 7 or 8 AM) less than 50 should probably be planted 1.25 to 1.5 inches deep, and corn at least 1.5 inches deep. When planting into warmer soils later in April or in May, 1.5 inches is good for soybeans and 1.75 inches for corn. Manually changing planting depth on a 24-row planter is good exercise, but may not always be worth the time it takes. As long as we’re planting between 1.5 and 2 inches deep, it’s not clear that trying to fine-tune depth based on current and future soil conditions has much potential to improve stands.

Especially when planters move at speeds of 6 mph or faster and when the soil surface is not very smooth, some seeds end up shallower and some deeper than the nominal setting. Equipment and seed companies have looked at the effect of planting depth on stands and yields, and have in some cases managed to produce large yield differences by employing “mistake” settings. Measuring the uniformity of seeding depth by digging up seeds is difficult, but high-speed cameras can estimate depth as seeds drop and settle in place. One study done by digging up corn roots at maturity reported a standard deviation of about an eighth of an inch, which would mean that about 5 percent of seeds would be at least a quarter of an inch shallower or deeper than the average. That’s probably acceptable at normal planing depths. More weight and more uniform down-pressure have improved planting depth uniformity, and if 75 percent or more of plants emerge over a period of about 15 growing degree days (24 hours at average temperature, longer than that if it’s cool) and the rest within one more day, it’s unlikely that any yield has been lost due to non-uniformity of planting depth.

Uniformity of distance between seeds is good enough to maximize yield potential in most fields, and needs no further mention. Despite what yield contest winners say they do, there is no reason for most people to plant slower than they do now. If the monitor says enough seeds are being dropped, and either the monitor or previous experience (by seeing how stands look after emergence) say they’re spaced uniformly enough, they probably are.

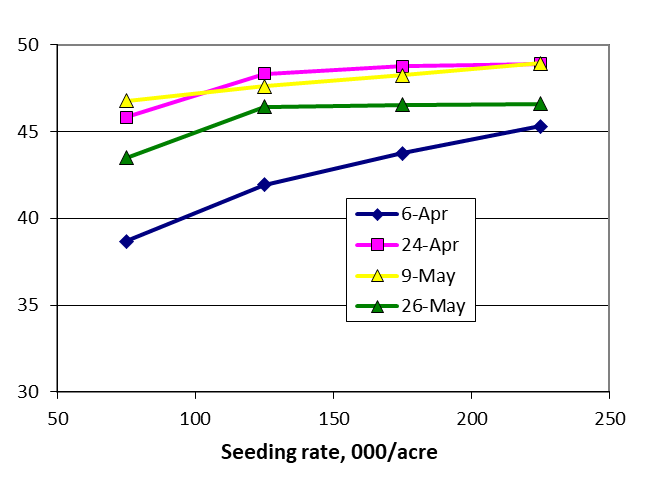

Seeding rate

Most people have decreased the number of soybean seeds dropped per acre over the past decade or so, but seed quality has also improved, and so the number of plants needed to maximize yield has probably not decreased as much as the seeding rate. We know that seeding rate responses are highly variable: in a series of 25 seeding rate studies in Illinois between 2015 and 2018, we found that the stand (not seed) numbers needed to maximum dollar return to seed ranged from 50 to 200 thousand, and there was no correlation between yield and plant stand needed to produce that yield. That means that the best way to set seeding rates is to average over seeding rate trials to get a best-guess prediction.

Averaged over the 25 responses, the plant stand needed to maximize the net return to seed was about 107,000 plants. At 80% stand establishment, that would require planting 134,000 seeds per acre. While that seems like a reasonable seeding rate, the “best” seeding rate was higher than that in about half of the trials and less than that in the others. Responses were fairly flat in most of the trials, though, which says that moving around within a range of 125,000 to 145,000 seeds per acre won’t miss the mark by much. If you expect emergence to be higher than 80%, seeding rates can be decreased. If you’ve gotten good yields planting only 100,000 or 110,000 seeds in the past, feel free to do that again. Keep in mind, though, that yield responses to seeding rate may not be very visible. So while 100,000 seeds might produce a good yield of 75 bushels, using 130,000 seeds might increase that by 2 bushels, which won’t look like much but would increase profits by $12–13 per acre.

The response of corn to plant population is much more consistent that for soybeans. Figure 3 below shows the response to corn plant population over 44 trials in Illinois between 2012 and 2018. Each trial included four to six hybrids, with planted populations ranging from 18,000 to 50,000 per acre. Final stand closely matched seeding rate, so they’re used interchangeably. The average yield at the 100% (of maximum) yield level was 237 bushels per acre. We used a wide range of seeding rates in order to produce visible responses, even though we know that this range extends far outside the range that producers might consider. Yields at 48–50,000 plants were lower than those at 34–36,000. So what we chose as the high end of the range ending up “bending” the curve, which changed where it reaches a maximum. The curve fitted to yields from the populations up to and including 42,000 shows that the maximum yield was produced at 36,900 plants per acre, and the optimum population—where the last seeds added were paid for by the increase in yield—was 33,400 plants per acre.

Figure 3. Corn plant population response over 44 trials in Illinois, 2012–2018.

Figure 3. Corn plant population response over 44 trials in Illinois, 2012–2018.

It’s also worth noting that, although we find best returns from plant populations in the 32,000 to 35,000 per acre, having them a few thousand higher or lower is not going to change yields or net returns by very much. Yield level doesn’t make much difference: yields in 2012 were about 50 bushels lower than in the highest-yielding years of this study, but the population response was about the same as in other years. Going up to 40,000 isn’t very likely to increase yields, but it won’t increase costs much, either, so it won’t do much harm in productive soils. Marlin Jeschke of Pioneer recently reported that harvest populations for non-irrigated entries in the NCGA Corn Yield Contest over the past five years was 36,700, so it’s clear that current hybrids don’t don’t require unusually high populations to produce high yields.

If planting is delayed in 2020

Should management of corn or soybean change if planting is delayed in 2020 like it was in 2019? We’re certainly hoping that any delays are not on the scale that we saw in 2019, but we did not see many signs last year of things we should change if planting is late in 2020. That may have been because of good weather and good yields even after the late planting. About the only thing we might want to consider if corn planting is delayed into June is to move to earlier–maturing hybrids in the northern part of Illinois. Hybrid strip trials planted in that region in early June last year showed lower yield for hybrids later than 107–108 days RM. We did not see this with late-planted soybeans there, nor for either corn or soybeans in central and southern Illinois.