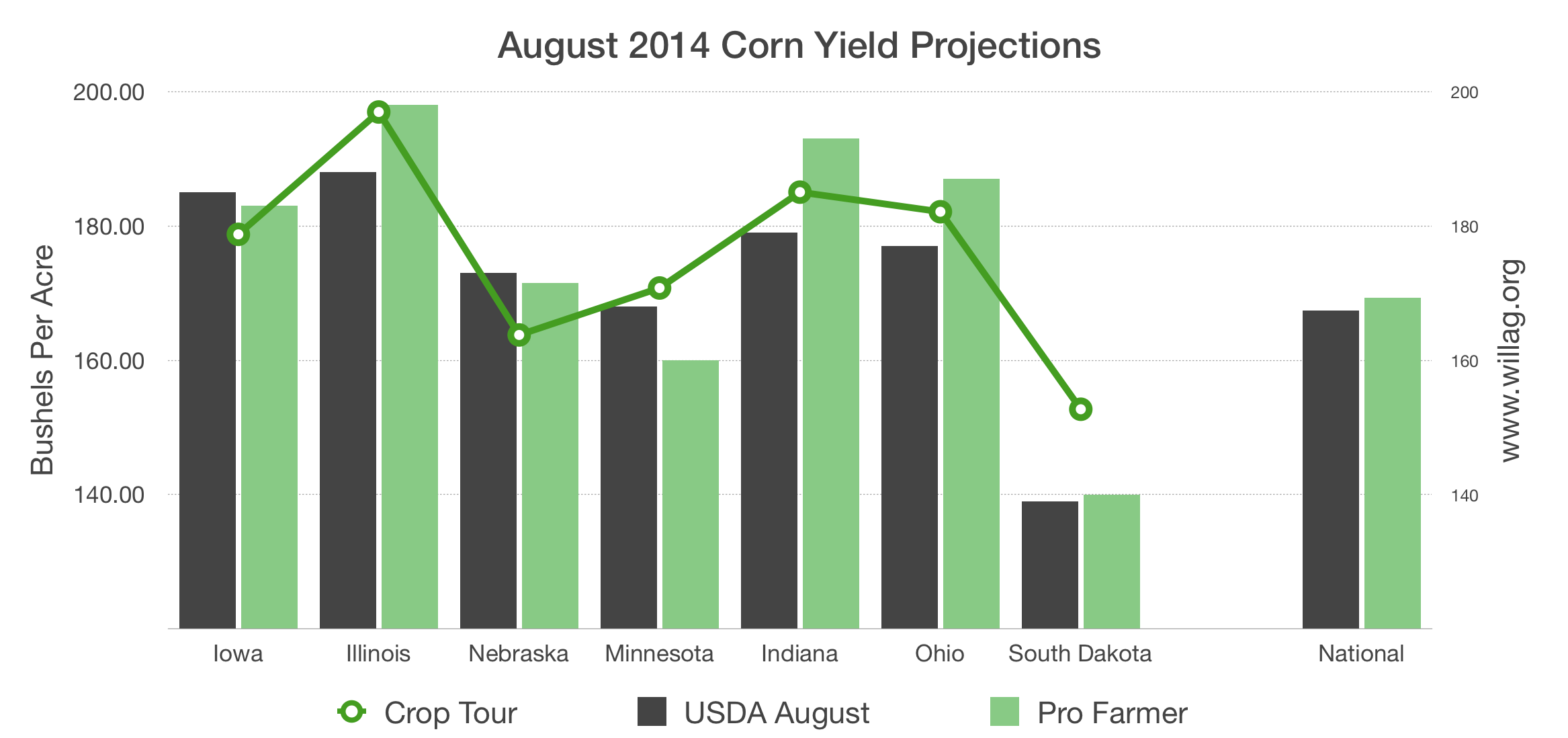

The March 31 Grain Stocks Report

The reports USDA releases March 31 will set the tone of agricultural trade for three months in Chicago.

Once every quarter the National Agricultural Statistics Service takes a census of the available bushels of corn, soybeans, and wheat. It is called the Grain Stocks report. It is not exactly a survey, but rather more of an actual accounting, in his case of what’s stored in Illinois, says NASS State Statistician Mark Schleusener, “…to measure the whole supply of grains and oilseeds USDA NASS does on farm surveys. Those are done with producers to find out what they have in their grain storage bins. Off farm storage tallies bushels in the mills and the elevators using a census as of March 1. All commercial storage facilities are contacted”.

Nationwide more than 9000 commercial storage facilities are contacted for the census side of the Grain Stocks report. The survey side - that done with farmers - is sent to more than 80,000 producers with an 80 percent response rate. The goal is to get a very accurate accounting of the bushels available for use.

Where the bushels are stored changes across the season. December 1 it is stored on farm. Through the winter months these bushels slowly move to the elevators and mills and eventually, in the case of corn, the bushels are shipped down the river for export, or fed to livestock, or turned into ethanol. The bushels are used.

If you add what’s used to what’s left - the Grain Stocks number - the sum should be the total available supply for the year. However, tracking the middle usage number for corn - bushels fed to livestock - isn’t possible. That’s why USDA calls this number Feed & Residual. This season it is supposed to be 5.3 billion bushels. The question is how much of that 5.3 billion has already been consumed. There in lies the guess says University of Illinois Ag Economist Darrel Good.

The Grain Stocks report for corn has a wide range then of acceptable figures from around 7.4 to 7.7 billion bushels. It makes the Grain Stocks number not so important, and puts a great deal more weight on the Prospective Plantings report to be released on the same date, March 31.

Once every quarter the National Agricultural Statistics Service takes a census of the available bushels of corn, soybeans, and wheat. It is called the Grain Stocks report. It is not exactly a survey, but rather more of an actual accounting, in his case of what’s stored in Illinois, says NASS State Statistician Mark Schleusener, “…to measure the whole supply of grains and oilseeds USDA NASS does on farm surveys. Those are done with producers to find out what they have in their grain storage bins. Off farm storage tallies bushels in the mills and the elevators using a census as of March 1. All commercial storage facilities are contacted”.

Nationwide more than 9000 commercial storage facilities are contacted for the census side of the Grain Stocks report. The survey side - that done with farmers - is sent to more than 80,000 producers with an 80 percent response rate. The goal is to get a very accurate accounting of the bushels available for use.

Where the bushels are stored changes across the season. December 1 it is stored on farm. Through the winter months these bushels slowly move to the elevators and mills and eventually, in the case of corn, the bushels are shipped down the river for export, or fed to livestock, or turned into ethanol. The bushels are used.

If you add what’s used to what’s left - the Grain Stocks number - the sum should be the total available supply for the year. However, tracking the middle usage number for corn - bushels fed to livestock - isn’t possible. That’s why USDA calls this number Feed & Residual. This season it is supposed to be 5.3 billion bushels. The question is how much of that 5.3 billion has already been consumed. There in lies the guess says University of Illinois Ag Economist Darrel Good.

Quote Summary - If the most recent pattern is being followed this year and USDA’s 5.3 billion bushel usage for the year is correct, then use for the first half the year should total 3.9 billion bushels with 1.7 of that used in the second quarter. If that is the case, the total use during the second quarter would have been 3.75 billion bushel and leave March 1 stocks at 7.45 billion.On-the-other-hand, if the usage pattern is more like it was prior to 2010, there could be another 200 or 300 million bushels of corn accounted for in the Grain Stocks figure because it hasn’t yet been consumed. It will still be consistent with a 5.3 billion bushel usage figure for the year.

The Grain Stocks report for corn has a wide range then of acceptable figures from around 7.4 to 7.7 billion bushels. It makes the Grain Stocks number not so important, and puts a great deal more weight on the Prospective Plantings report to be released on the same date, March 31.